Injured in an accident, and now you need to borrow money on your case? Accident lawyers are not allowed to loan money to their clients, but you can get a “loan,” called a lawsuit cash advance, from a lawsuit settlement advance funding company.

What Is a Lawsuit Pre-Settlement Loan?

The money you receive from a lawsuit funding company is not a loan!

Loans are usually repaid monthly and have to be paid back no matter what. A cash advance from a lawsuit funding company is only paid back at the end of your case and does not have to be paid back at all if your case loses.

The money that a lawsuit funding company provides is a cash advance of a portion of your settlement. The technical name for a lawsuit cash advance “loan” is a non-recourse note.

The lawsuit funding company pays you to purchase your right to a portion of the lawsuit award or settlement in the future.

This allows lawsuit funding companies to charge very high interest rates, which they need to offset the times when they lose their money. Sometimes, cases are lost. Sometimes, clients pass away before settlement, and the case value decreases substantially. Remember, the funding company only gets paid back if your case settles for enough money to pay them back.

When Can I Borrow Money On My Accident Case?

You can borrow money any time after you retain a lawyer for your accident, even before a lawsuit is filed. However, your lawyer will first have to obtain medical records showing your injury and some other records to provide to the lawsuit loan company.

How fast you can borrow money on your accident case depends on how fast you call a personal injury lawyer, how much of your medical treatment you have had, and how fast your lawyer can get your medical records and investigative reports.

Why Doesn’t My Personal Injury Lawyer Want Me to Get a Lawsuit Loan?

Many lawyers do not want a client to get a lawsuit loan because if the client owes too much money, the client will want to demand a bigger settlement and decline a reasonable settlement offer. This can force a case to go to trial, which is risky.

We will gladly get you a lawsuit loan if you need it.

How Can I Get a Lawsuit Loan Without an Attorney?

Unfortunately, without an attorney, you cannot get a lawsuit loan (cash advance). There are three reasons why you need a lawyer to get a lawsuit loan (cash advance):

- Without a lawyer, you will never get a reasonable settlement. A lawsuit loan company will not advance money to you unless they believe the company will be paid back. They know you will not be able to settle your case for enough money to repay the cash advance if you are not represented by a lawyer.

- A lawsuit loan company needs your lawyer to provide a copy of the following: police report, insurance information, a letter from the insurance company acknowledging the claim, hospital records, and medical records to determine if they want to give you money. In some cases, a lawsuit loan company may require additional documents and

- A lawsuit loan company needs your lawyer to guarantee repayment if your case is settled.

What Can I Do If My Personal Injury Lawyer Can’t Get a Cash Advance?

If your lawyer cannot get a lawsuit loan company to give you a cash advance, you can call lawsuit loan companies directly.

Most personal injury lawyers deal with only one or two lawsuit loan companies, but there are many. If you look on Google and call several lawsuit loan companies, you may find one willing to give you a cash advance. They will then call your personal injury lawyer.

How Much Money Can I Borrow On My Accident Case?

You cannot borrow as much as you want or as often as you want.

The lawsuit cash advance company we use for most personal injury cases will loan or advance up to 10% of the amount they believe your personal injury case is worth.

One lawsuit cash advance company, Law Cash, will loan or advance up to 10% of the amount of the insurance policy or up to 10% of the amount they believe your personal injury case is worth, whichever is less. A lawsuit cash advance company will use a conservative settlement value for your personal injury case.

Some lawsuit cash advance companies are more conservative and will advance a little less than 10%, and some companies will advance a little more than 10% of the estimated value of your personal injury case. Additionally, different lawsuit cash advance companies will estimate the value of your personal injury case at different amounts.

Lawsuit cash advance companies will evaluate the value of your personal injury case and not give you any amount you or your personal injury lawyer wants. The lawsuit cash advance company we use has an underwriting department headed by a former personal injury lawyer.

How much is your personal injury case worth? To find out what your personal injury case is worth and how much you can borrow from a lawsuit cash advance company, you’ll have to decide how much you need and ask your personal injury lawyer to request a cash advance. This is because there are no good personal injury settlement calculators available. They are all designed only to get your personal information. Read more about personal injury settlement calculators.

You can also use our lawsuit loan calculator below.

Example of How Much You Can Borrow On Your Accident Case

These examples are given for illustrative purposes and may not be accurate because I have never worked for a lawsuit cash advance company, and every lawsuit cash advance company operates differently.

Example 1: Assume the lawsuit cash advance company evaluates your injury to be worth $50,000 and the insurance policy is $100,000; you will be able to receive a maximum of $5,000.

Example 2: Assume you are injured in an accident, and your personal injury attorney believes your case is worth $500,000, and there is enough insurance to pay that amount. The lawsuit cash advance company may put a value of $250,000 on your case for the purpose of the cash advance.

You ask for and receive a $15,000 cash advance on your personal injury case 2 months after your accident.

6 months later, you ask for and receive another cash advance in the amount of $5,000. You have now received a total of $20,000.

6 months later, you ask for another cash advance in the amount of $15,000.

It is likely that you would only be able to receive another $5,000, which brings the total advanced to $25,000, which is 10% of the $250,000 value estimated by the lawsuit cash advance company

How Many Times Can I Borrow Money Again Against My Accident Settlement?

After you have borrowed money against your personal injury settlement once, you may be able to get more money from cash advances if your case is worth enough to settle. We have had clients who borrowed money multiple times.

While additional loans can be made, the total of those loans and interest will still be subject to the maximum amount that the lawsuit cash advance company is willing to loan.

Can I Get Money in a Lump Sum or Monthly?

If you want money all at once, you can get that. If you want the money paid to you monthly over a period of months, it can be sent to you monthly over 6-12 months. After that, you can request another cash advance.

You might want the money paid to you monthly so you can pay rent, car payments, and/or health insurance premiums to pay for surgery.

When Can I Be Denied By a Lawsuit Funding Company?

Three reasons you could be denied a lawsuit loan:

When It’s Too Early

Your personal injury case may not be ready yet for a lawsuit cash advance company to give you money. If the documents required by the lawsuit loan company are not yet available to your lawyer, you may be temporarily denied.

For instance, your personal injury lawyer may not have obtained a police report, hospital records, or medical records yet.

If You Don’t Have a Good Personal Injury Case

If your personal injury case doesn’t meet the criteria required by the lawsuit loan company, you will be denied. However, this is not common. If your case is good enough for a personal injury lawyer to represent you, then a lawsuit loan company will likely agree that you have a good case and will advance you some money.

We have had personal injury cases that were turned down by three other lawyers, like when our client ran a red light or admitted he ran a stop sign. We settled those cases for the entire insurance policy of $100,000, but it’s unlikely you would get settlement advance money on a case like that.

If You Already Borrowed Too Much on Your Personal Injury Case

If you haven’t borrowed money on your accident case yet, you are unlikely to be declined a cash advance.

If you were declined additional cash advances because your lawsuit cash advance company says you owe too much, another lawsuit advance company might loan you money at a higher rate, but they will have to pay off your first loan, and all the money you borrowed will now be at the higher rate. Eventually, you won’t be able to borrow any more money.

You cannot go to another lawsuit cash advance company and borrow money from them without telling them you already have a previous cash advance. That won’t work because:

- you would be committing fraud;

- your lawyer cannot hide the fact that you previously received a cash advance, and

- the cash advance company will find out anyway.

Lawsuit cash advance companies use a nationwide clearing association to check if you have already obtained money against your lawsuit.

When you request a cash advance, they will run a “credit report” to see if you have received money from any other lawsuit cash advance company. They will even look at previous cases where you received money to see if there were any problems.

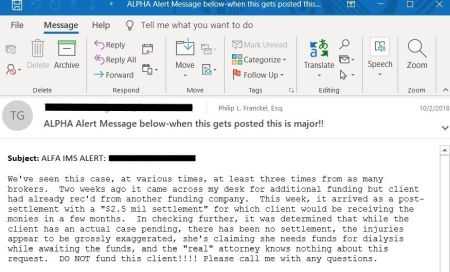

This image shows an email sent to our law firm from a lawsuit cash advance company when they denied a cash advance to our client. They emailed us a copy of the “ALPHA IMS ALERT” which indicates what was reported to the nationwide clearing association about the client’s previous lawsuit funding.

Lawsuit Cash Advance Funding ALPHA IMS ALERT

How Long Does It Take to Borrow Money On My Accident Case?

We can usually get approval in 2 hours and money for you within one day. We are a LawCash (Cartiga) VIP personal injury law firm that allows us to get your money faster and at a preferred lower rate!

Call the HURT911® Personal Injury Dream Team™ right now 7 days/nights for a free consultation with no obligation at

1-800-HURT-911

1-800-487-8911

You can change your personal injury lawyer anytime.

Why Is It Taking So Long for My Lawsuit Loan to Get Approved?

If there is more than one day delay in getting your lawsuit loan approved, it is likely because the required documents weren’t yet available or you have a personal injury attorney who does not like lawsuit loans.

Continue reading below this section

![]()

Injured? Call 1-800-HURT-911® New York’s Personal InjuryDream Team™ right now 24/7 for your free consultation to protect your rights!

Injured? Call 1-800-HURT-911® New York’s Personal InjuryDream Team™ right now 24/7 for your free consultation to protect your rights!

We’ll call you back within minutes!

1-800-487-8911

![]()

![]()

No Win — No Fees

— GUARANTEED! ™

![]()

See how Nyda got her dream house! What will you do with your settlement money?

![]()

What Is Needed for a Lawsuit Loan?

You will need the following to get a lawsuit loan (lawsuit cash advance):

- Be represented by a personal injury lawyer who is willing to cooperate with the lawsuit cash advance company.

- Document showing how the accident happened with reports, such as a police report, ambulance report, incident report, urgent care record, hospital record, and medical records from a doctor.

- Proof that the person or company responsible has insurance and policy information.

- Medical record showing what your injury is.

Can I Get Money Every Month?

Yes. We can arrange for you to get a lawsuit settlement advance payment every month for up to 12 months. After 12 months, if you still need money, you will have to reapply.

Can I Get Cash, or Do I Have to Get a Check?

No. With at least one lawsuit cash advance funding company we use, you can get your money by any of the following:

- Debit card

- Check or

- Cash

Esquire Bank, located in Brooklyn on Court St, can give you use their MasterCard debit card and deposit all of the money to your debit card or deposit money every month to your debit card.

Lawsuit Cash Advance Debit Card

If you want cash, you can cash the check they give you at Esquire Bank in Brooklyn. You would pick up a check at their office and cash it at Esquire Bank in the same building.

Is It a Good Idea to Borrow Money Against My Accident Case?

It may be a good idea to get a lawsuit cash advance when you need money to pay:

- Medical treatment

- Rent

- Mortgage payments

- Car payments

- Other living expenses

If you’re considering borrowing against your 401(k) account, you should instead consider borrowing against your lawsuit.

If you’re considering borrowing against the equity in your house, you might instead want to consider borrowing against your lawsuit.

Borrowing money for medical treatment, especially surgery can make sense when you need medical treatment. The additional medical treatment will likely make your case worth more money than what you have to pay back.

A lawsuit loan makes sense when you want to accept a low settlement offer because you need money. A lawsuit loan can allow you the additional time your lawyer needs to get a larger settlement offer.

Example: The insurance company offers you a settlement of $60,000 for your torn meniscus with arthroscopic surgery. You need $5,000 now, so you want to settle. Instead, you can borrow $5,000 and take your case to trial. Even if you have to pay back $17,500 for your lawsuit loan, you’re still way ahead if we can get you a lot more money.

Real-life example: GEICO offered our client a settlement of $10,000 for a torn meniscus with arthroscopic surgery. Our client borrowed $5,000 from LawCash to help pay the bills while he was recuperating from knee surgery. When the trial was finished five years later, $17,500 was paid back to LawCash. Because he did not have health insurance, his surgery and therapy were done on a medical lien, and $8,400 was paid back to the doctors for medical treatment from the money awarded at trial. We obtained a jury verdict of $465,000 for his knee injury, so even though he had to pay back $25,900 on his lawsuit loan, he was still way ahead.

However, the interest rate charged on lawsuit funding loans is substantial, and it doesn’t make sense to borrow money unless it’s an emergency. But almost everyone has emergencies, and things just get worse after an accident!

What Can I Use the Money From My Lawsuit Advance For?

You can use the money for anything you want, but it’s best not to borrow money if you can avoid it because it will cost you 2-4 times more money to pay back by the time your case is finished.

If you need to borrow money, we recommend using it to pay for the following:

-

- Rent

- Mortgage payments

- Car payments

- Health insurance

- Medical treatment

- Surgery

- Veterinary bills (I include this because my pets are more important than me!)

- Avoiding bankruptcy

If you use the money to pay for medical treatment or surgery related to your accident or health insurance that you use for medical treatment of your injuries, it can increase the value of your case many times more than the cost of interest when you have to pay back your cash advance.

Can I Use Money From a Lawsuit Loan to Pay off Credit Cards?

Using the money from a lawsuit loan to pay off your credit cards is not a good idea unless you want to avoid ruining your credit, which has a credit score of 675 or more. Credit cards usually have a lower interest rate than a lawsuit cash advance.

Can I Use Money From a Lawsuit Loan to Avoid Filing for Bankruptcy?

Yes. Using the money from a lawsuit loan may be a good idea to avoid filing for bankruptcy.

If you file for bankruptcy, the bankruptcy court will appoint a trustee in bankruptcy who will take over your case. The bankruptcy trustee has the right to hire a new lawyer for your case and can even settle your case without your permission and take your money!

The trustee doesn’t care how much money you receive. The trustee will only care about getting money from your settlement to pay back your creditors. Basically, your case is an asset that can be used to satisfy creditors to whom you owe money.

What Is the Maximum Interest Rate Allowed to Be Charged for a Lawsuit Loan Advance?

Loans are subject to maximum interest rates regulated by the state. However, the maximum interest charged for a cash advance lawsuit “loan” is not regulated in New York because it is not a loan (see above).

Since a cash advance is not a loan, lawsuit funding companies typically charge interest rates of 3% – 4% per month, equaling 36% – 48% annually.

We are a LawCash VIP personal injury law firm, which allows us to get your money faster and at a preferred lower rate, usually 2.5% monthly interest. We can often get approval in 2 hours and money for you within 1 day. For a free consultation, call us 7 Days/Nights at 1-800-HURT-911 > 1-800-487-8911.

Lawsuit funding companies can charge whatever interest rate they want, so you should compare lawsuit funding companies carefully.

Rates change from company to company, and even within the same lawsuit funding company, there will be different rates depending upon the risk involved with your case, your injury, the amount of available insurance, and who your accident attorney is.

Other factors besides the interest rate will increase the cost or the amount you have to pay back.

How Much Will It Cost Me to Pay Back If I Borrow Money on My Lawsuit?

Generally, you will probably pay back 2-5 times the amount you borrow, depending on how long it takes to settle your case.

Even if your case is settled soon after your cash advance, funding companies will usually charge a minimum of 6 months interest, even if you repay the “loan” a month after you borrow the money.

Some cases can be settled within a few months. For instance, if you have a broken leg in a car accident, bicycle accident, or motorcycle accident and the other car has a $100,000 insurance policy, your case could probably be settled within 2-3 months, and you won’t need a lawsuit loan.

New York personal injury cases that can’t be settled typically take 3-5 years to reach a trial. While it’s possible that a case could be settled in the first year or two, in the last few years, insurance companies have frequently refused to make any settlement offer until the case is near trial.

Personal injury cases against New York City and New York City government agencies typically take 4-7 years to reach a trial.

It often takes approximately 1.5-3 years for your lawyers to finish working on a New York accident case. When your attorney notifies the NYS Supreme Court that your case is finished, your case then goes on a “line,” waiting for the court to have a judge available for trial. It’s like waiting at the DMV, only much longer! The waiting period for a trial is typically 1.5-2 years.

The total time to reach a trial after first seeing an attorney for your accident is approximately 3 to 5 years.

One of our clients insisted on borrowing $15,000 to buy a motorcycle. When the case was settled for the entire $250,000 insurance policy, the repayment amount was $52,000. We got it reduced to $42,000, but that could’ve bought a really nice motorcycle.

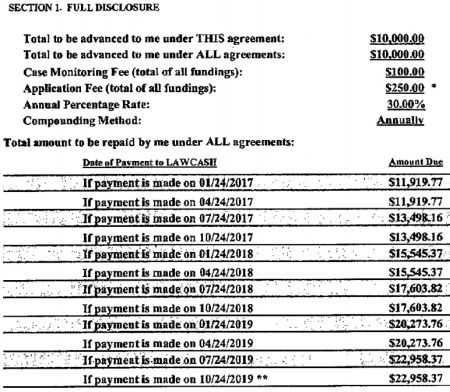

Before you sign the final papers to borrow money against your settlement, review the payback schedule that the lawsuit funding company provides you. The payback schedule will show you the amount you must pay back on different dates.

This payback schedule shows the amounts due at 4-month intervals. $10,000 was borrowed on 10/27/2016 at 2.5% per month for a total of 30% annually. If the loan is paid back any time within the first 12 months or before 10/27/2017, 12 months of interest is due. If the loan is paid back three years after borrowing, the payoff amount is $22,958.37.

Many clients said they would pay the money back before their case was settled, but no one ever has. If you need to borrow money on your case, just be prepared to have a lot of money deducted from your settlement to pay back your loan.

Lawsuit Loan Calculator — Calculate What a Lawsuit Loan Will Cost

It is often worth borrowing money on your accident case if you don’t need a lot; you could get a lot more money by settling later, and you’re borrowing the money for a good reason, not for a new TV.

If you’re borrowing money to pay for surgery, that will probably increase the value of your case more than the amount you have to pay back. Your lawyer can help you determine if it is good for you.

Use our lawsuit loan calculator to find out what one or multiple lawsuit cash advances will cost you and compare one lawsuit loan vs another lawsuit loan. Factors computed by this calculator include how often the rate is compounding, origination or underwriting fee, monitoring fee, compounding method, and rates.

We often obtain lawsuit funding for 30% annually, but many law firms work with lawsuit cash advance companies that charge 36%-50% annually. Some law firms refuse to work with lawsuit cash advance companies. If your lawyer refuses to work with a lawsuit cash advance company, your only option is not to borrow money or retain a new lawyer.

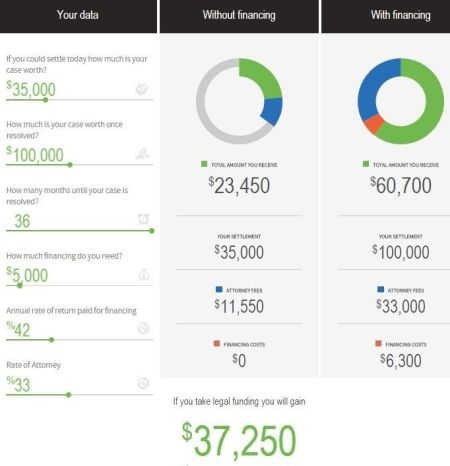

This screenshot of a lawsuit funding company’s calculator shows an example of borrowing $5,000 over 36 months at 42% interest for an accident case with an early settlement offer of $35,000 versus a $100,000 settlement value just before trial. This assumes that the trial of the case is 3 years after borrowing the money. Without including fees, you would get an additional $37,250 by borrowing $5,000 so you could settle 3 years later.

How Will My Settlement Loan Be Paid Back? Do I Have to Make Payments?

You will not have to make monthly payments. You won’t actually make any repayment. Your lawyer will repay the amount owed out of your settlement money when your personal injury case is settled.

How to Compare Lawsuit Cash Advance Funding Companies?

Use our lawsuit loan calculator to compare one lawsuit loan vs another lawsuit loan.

Look At the Following to Compare Lawsuit Loans:

-

-

- Monthly interest rate

- Interest rate period

- Compounding

- Underwriting fee

- Annual monitoring fee

-

Monthly Interest Rate —

The monthly interest rate is just that. Lower is better. A monthly interest rate of 3.0% instead of 3.5% equals a 6% lower annual rate.

Interest Rate Period —

This refers to the period of time the interest will be charged. For instance, if your loan is paid back 13 or 14 months after you borrow the money, you may have to pay 18 or even 24 months of interest.

There will be a minimum amount of interest time charged. Most lawsuit funding companies charge a minimum of 12 months of interest, after which the minimum period of time could be 6 or 12 months.

For instance, if you repay your loan two months later, you may still have to pay 12 months of interest. If your lawsuit loan company charges a minimum of 12 months of interest and a minimum of 6 months after that, you will pay 24 months of interest if your loan is paid back more than 18 months after you receive the money.

Compounding —

Compounding is the interest calculated on the initial principal and also on the accumulated interest of the previous periods. You will want to know if the interest is compounded monthly, bi-annually, or annually.

The more frequently the interest rate is compounded, the more it will cost you. In other words, annually is best.

Underwriting Fee —

The underwriting fee is a one-time charge, usually $250-$750, to review your file, including investigative materials such as a police report, medical records, and other records to determine how much the lawsuit funding company will loan you.

Annual Monitoring Fee —

This is usually a small one-time or annual fee to monitor your case, communicate with your attorney to determine the progression of your case, and make sure that the lawsuit funding company gets paid back.

Reasons Not to Borrow Money From a Lawsuit Funding Company

-

-

- You want to borrow money for a new motorcycle. One of our clients insisted on borrowing $15,000 for a new motorcycle that cost $45,000 at the end of her motorcycle accident case.

- The interest rate charged is higher than credit card interest rates.

- When you decide to accept a fair settlement offer from the insurance company, which could be the entire insurance policy, you may find that you’re not getting much money after all the interest is paid on your lawsuit “loan.”

- Because the interest owed accrues so quickly, you may feel pressured to settle your case prematurely for much less than it’s worth.

- When the insurance company offers a realistic settlement offer, which is usually at the time of trial, the interest owed may be so much that you don’t want to settle and make risky decisions because of the amount you owe.

- The lawsuit funding company requires confidential information about you and your accident, such as your medical records and other records, so they can evaluate your case. This waives the attorney-client privilege and may waive the work product privilege, which means the defense may be allowed to obtain copies of the lawsuit funding company records. The lawsuit funding company may even provide the defense with their written evaluation of the case, showing an amount much less than your case is really worth, making it more difficult to settle.

-

Medical Financing

Medical financing is a loan you obtain to pay for medical treatment or surgery. Medical loans may be obtained from a medical financing company through your doctor or by a lawsuit financing company.

Should You Borrow Money Against Your Lawsuit to Finance Medical Treatment or Surgery?

If you have medical insurance, it will always cost you less to go through your insurance.

Sometimes, an accident victim may not have health insurance or prefers to receive surgery from a particular doctor who doesn’t accept your health insurance. In this instance, medical financing can be appropriate. Surgery will increase the value of your case.

What Is the Difference Between a Lien and a Loan?

Another choice is to ask your doctor to provide treatment on a lien. A lien is an agreement signed by you and your lawyer that promises to pay your doctor at the end of your case.

With a lien, usually, no interest will be paid. Only the principal will be paid to your doctor at the end of your case. You must repay the principal with interest with a loan or medical financing.

Usually, a lien is contingent upon the settlement of your case. If it is contingent upon settling your case, you will not have to pay it back if your case doesn’t settle. We just received a lien from a doctor who will do surgery, and the lien is not contingent, which means our client will have to pay it back whether his case settles or not.

Your doctor may agree to provide medical treatment on a lien, or when surgery is needed, your doctor may agree to a partial lien with partial medical financing.

Difference Between a Loan From a Medical Financing Company Versus a Loan From a Lawsuit Funding Company

A loan from a medical financing company will not be repaid from the settlement of your lawsuit. This type of loan is called a recourse loan, and it is a real loan. The interest rate will be subject to usury laws and will, therefore, have a lower interest rate. It will have to be paid back if you lose your lawsuit.

A medical loan from a lawsuit funding company will be repaid from the settlement of your lawsuit. This is the same as the lawsuit funding for personal reasons. It will be at a higher interest rate but will not have to be paid back if your lawsuit is unsuccessful.

How to Create a Budget, Know How Much You Need to Borrow, and Borrow Less

Use a budget template to see how much money you need to live, where you can reduce your expenses, and how much money you will need to borrow on your accident case.

This article at the Huffington Post reviews 5 household budget templates. The templates use Excel spreadsheets. If you don’t have Microsoft Excel, you can download the entire Office Suite for free.

![]()

![]()

Attorney Philip L. Franckel, Esq., personally authored this page and all articles on NYSeriousInjuryAttorneys.com.

Attorney Philip L. Franckel, Esq., personally authored this page and all articles on NYSeriousInjuryAttorneys.com.

Phil Franckel is a well-known personal injury lawyer in New York since 1989. He is a Founding Partner of 1-800-HURT-911, LLP®, the Personal Injury Dream Team™, and a former Member of the Board of Directors of the New York State Trial Lawyers Association. He has an Avvo Top 10 Rating, Avvo Client’s Choice Award with all 5-star reviews, Avvo Top Contributor Award, Multi-Million Dollar Trial Lawyers Award, and others. See Mr. Franckel’s bio for areas of expertise.

![]()

Get the 1-800-HUR-T911® Dream Team™ on your side and become a member of our family!

We’ll immediately protect you from the insurance companies!

“Knowing I had a team of great lawyers on my side gave me a sense of power and peace of mind. They took care of everything for me. When a settlement was negotiated, I saw the difference a team of lawyers makes.”

—Lia Fisse

No Win — No Fee — No Expenses — Guaranteed!

Attorneys who can get you the most amount of money AND provide personal service!

![]()

![]()

Please take a look at some of our:

What will happen when I call 1-800-HURT-911 or chat?

- Our call center operators and chat operators are available 24/7.

- Just give your contact info to our operator and Founding Partner Rob Plevy, Esq. will call you within 5-10 minutes for your free, no-obligation consultation during the hours of 8 am – 10 pm. After hours, Rob will call you in the morning or at the time you want.

- Then just text or call us any time you want during your case!

Because any delay could cause you to lose viable rights and benefits, please call HURT-911® Founding Partner Rob Plevy, Esq. right now for a free consultation to find out your rights days/nights/weekends.

1-800-HURT-911

1-800-487-8911

You can speak, text, or email with us whenever you want throughout your case and afterward, days/nights/weekends, and experience our famous personal service. You’ll even get our personal phone numbers so you can call or text anytime!

Watch Founding Partner Phil Franckel, Esq. talk about New York Serious Injury Attorneys.com, difficult cases, and the 1-800-HURT-911® Dream Team™

Philip L. Franckel, Esq. is one of the HURT911® Dream Team™ Founding Partners at 1-800-HURT-911® New York; He has a 10 Avvo rating; Avvo Client’s Choice with all 5-star reviews; Avvo Top Contributor; and a former Member of the Board of Directors of the New York State Trial Lawyers Association.

Founding Partner Rob Plevy, Esq.

Robert Plevy, Esq. is one of the HURT911® Dream Team™ Founding Partners at 1-800-HURT-911® New York. Rob began his legal career in 1993 as an Assistant Corporation Counsel defending The City of New York against personal injury lawsuits.

Get the HURT911® Dream Team™ on your side!

Call Attorneys Rob Plevy & Phil Franckel days/nights/weekends for a free consultation

1-800-HURT-911

1-800-487-8911

![]()

![]()